General Mills

Overview

General Mills produces, distributes, and directly sells processed foods. The company manages over 100 brands, including Cheerios, followed by Nature Valley, and Betty Crocker. Since 2018, with the acquisition of Blue Buffalo, it has also been operating in the pet food industry. General Mills' most important brands sell worldwide, but most of the company's revenue still comes from North America. The appeal to consumers remains strong as for most of the brands they own, market share has remained unchanged or grown in the last three quarters.

Strategy and outlook

General Mills' management has emphasized two key points of its strategy in the last conferences it attended:

Increasing focus on direct distribution in North America, investing in digital channels and e-commerce;

Continuing to increase market penetration in pet food, which has already doubled since the acquisition of Blue Buffalo.

Furthermore, GIS continues to grow through acquisitions while strictly adopting its Accelerate Strategy, in which the company divests its slow-growth businesses. This increases the company's competitiveness and revenue.

As we’ve repeatedly seen, investors are rapidly moving their money onto safe stocks that won’t be affected by a recession, therefore, causing a drop in the other parts of the market. Some of these resilient stocks could include food companies, where their products are always in demand, no matter the state of the economy. This can be said with General Mills, as they have a diverse portfolio of over 100 different food brands along which includes some of the most popular cereal brands in the world.

One positive thing I see in this company is their investor base. Usually when it comes to these types of companies, investors invest for long term gains and don’t sell their shares after one good or bad report. General Mills is a great example of this as when looking at the future, this company will continue to thrive and dominate the market with the brands they own. So if the company comes out with a bad report that made their stock drop, the best option will be to buy more shares at this discounted price rather than selling what you already have. The second positive thing about the shares of this company is their % movement. The average movement after a quarterly result is usually between 2% to 6%. The reason why I consider this to be a positive thing is because it keeps the amateur and new investors away and only attracts the people who are in this company for the long term and know the fundamentals of GIS. Stocks with high % movements usually attract beginners as they think it’s a quick way to make money. At the same time you constantly have people selling or buying shares, depending on their loss or profits so predicting a movement based on the company results is irrelevant as the only thing people look for are their own quick gains.

The second reason why I want to long this company is because of their past performance. They have almost always beat the estimates which shows that their customer base and business strategies are strong enough that even in the worst environments, they are still able to do well. To further back up my point, back in December when they reported their results, their stock was at $80 and three months later, it has been able to maintain this price without them coming out with any sort of reports. This a great sign, specially in today’s environment as everybody is extra cautious with their investments and most stocks have gone down. At the end of the day, it doesn’t matter how good a report is if the investors don’t see a future in the company and now that we are entering a recession, many people have put their money into safer stocks such as GIS.

A good way of predicting how much of their products are selling would be by taking a look at grocery retail chains and seeing if they had an increased or decreased number of sales compared to last quarter. Although this doesn’t particularly mean GIS products are selling more as well, it still gives us a good understanding of the market. Looking at Walmart and Target where most of their product sales comes from, they both had an increased number of sales along with a beat in estimates. I expect a direct translation to GIS products as well considering that they are essential items customers need.

The third reason that I find to come to our advantage this quarter is the raised salary of customers considering that this is their first report after the new year. Although a 3% increase in their income may not mean much, it significantly increases their buying power when it comes to GIS products due to their low pricing. I’ve also seen many of their products in Iran, where it’s almost impossible to see anything that is coming from outside the country. Unlike other brands, they have customers in countries that almost no other company has so for example even if America is entering a recession, another country that they operate in could be going the exact opposite way which would make them have a higher number of sales. As said by Nassim Taleb, opportunities are rare, much rarer than you think and I believe right now is a great time to enter this market as there still hasn’t been a recession and it is a much safer option for investors to take out their money from other stocks now before the market drops.

GIS' share price has performed well in the last decade, gaining over 65% in this period.

As a producer of consumer staples, GIS has the opportunity to be a fantastic defensive choice for investors in 2023, with economic conditions remaining uncertain. What is interesting about GIS is that it has returned several thousand percent since it first joined the stock market, and has returned high gains above and beyond dividends consistently.

In the last decade, we have seen consumers increasingly choosing to incorporate vegetarian or vegan values into their lives. This looks to be more than just a trend, with a sustained shift in the way consumers look at food. Vegetarian and Vegan foods are seen as the healthy option, even when this may not necessarily be the case.

This looks to be an area of expansion for GIS with the business taking several noticeable steps to progress its involvement in the industry in recent years. For example:

Providing funding for start-up Everything Legendary, which produces meat-free alternatives.

The business was the first major company to use animal-free dairy, which is another segment for growth. 70% of consumers asked stated they would purchase real dairy products produced by fermentation technology instead of cows.

GIS has participated in an early funding round for a plant-based seafood business.

None of these actions are wholesale changes to their trading profile on GIS that will lift profits overnight but is a representation of where the business can go.

As discussed above, consumers are increasingly focused on healthy eating and alternatives to traditional foods. Although some have chosen vegetarian / vegan options, the majority of people shifting their consumption habits are choosing healthier options. For example, consumers are increasingly choosing breakfast bars rather than chocolate bars, or baked chips rather than fried ones.

Once again GIS is positioned well here. Leading their charge in this segment is Nature Valley and their expansion into fruit snacks, which are seeing healthy volume growth. Further, the business has many products which it can naturally transition into the healthy snacks segment, such as chips. GIS' U.S. snack segment is the fastest-growing unit of the business currently.

Even in GIS' Pet segment, Blue Buffalo is the no.1 Natural pet food brand and has grown at a CAGR of 15% since its acquisition

GIS produces household goods for consumers, many of which are regular purchases and a staple within their lifestyle. This comes at a marginally small cost to the consumer relative to their income. For example, I take a Nature Valley Bar with me to university on a regular basis. This currently costs 44p per bar however, after some research I found out that they used to be 31p a bar, that's a 42% increase. But have I stopped purchasing? No. The beauty of inelasticity is that as long as enough people act as I do, GIS will continue to have the same or increased number of sales.

Disadvantages

One of the biggest disadvantages that General Mills faces is the “lipstick effect”. In a recession, people are less inclined to buy name-brand cereals like Cheerios and brand-name organic pet food, as people will start buying off-brand items as wallets get tighter. This is a problem as “General Mills predicts there is US$2bn worth of growth potential in its US pet-food brand Blue Buffalo as the so-called humanization trend in animals continues. Pet food represents the food manufacturing giant’s fastest-growing category, with the US market making more than 95% of sales.” GIS’s biggest emerging sectors are organic pet food and vegan milk products, both of which are being heavily impacted as of late, with the latter being shut down. “General Mills winds up “animal-free” US dairy brand Bold Cultr. The company had reviewed its innovation portfolio and decided to deprioritize funding for the brand. A statement posted on Bold Cultr’s website this week read: “Dear fans and customers, with a heavy heart, we want to let you know that we are closing our doors as of 27 February 2023. G-Works regularly reviews its innovation portfolio and evaluates investment decisions. Recently, the difficult decision was made to deprioritize funding for Bold Cultr.” When a new thriving sector of a business gets shut down due to “prioritizing funding” it signals that the company’s pockets are being tightened, reducing innovation and increasingly depending on safety. That wouldn’t be a problem and would be considered a positive if we were looking at the stock on a long-term basis, but considering how high expectations are due to the last Earning Reports’ outlook, this doesn't look promising.

With how high the expectations have been set “the analysts have set the bar high, arguably because of the guidance, and there is a chance for a miss or weak guidance. Absent those events, price action is set to move higher from this level which would be a trend-following signal. The next hurdle for price action will be near the $84 level. A move above that should get the market up to an all-time high. A new all-time high could be around the corner if the company shows additional momentum in the results.” The alternative though is a rapid drop in share price. Now this confidence from GIS isn’t unwarranted considering that “General Mills (GIS) was the best-performing stock in the S&P 500 on Feb. 21 after the maker of Cheerios cereal and Blue Buffalo pet food boosted its outlook for fiscal 2023, which ends in May.” The issue is that “Dividend is low compared to the top 25% of dividend payers in the Food market. Annual earnings are forecast to grow slower than the American market.” What we’re left with is questioning whether GIS is really a solid option for those interested in entering the food market, and also whether or not the incredibly high expectations are met later today.

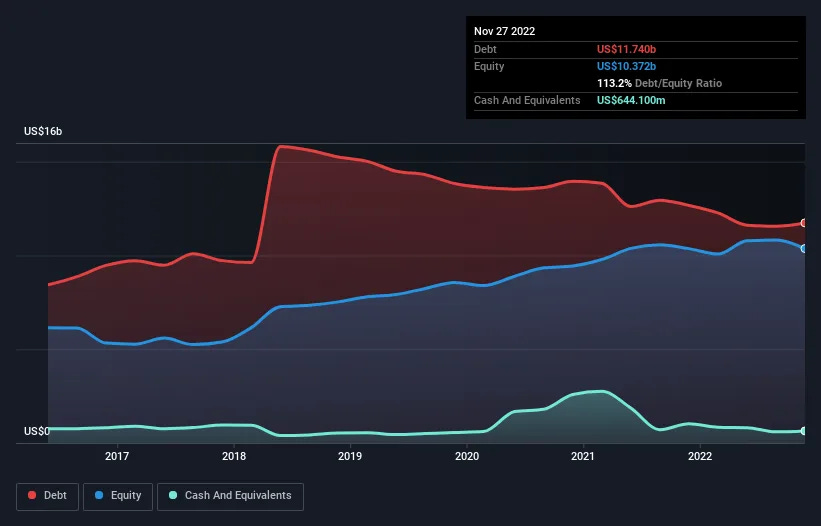

Another problem that GIS faces is its capital structure. “On the latest balance sheet data, we can see that General Mills had liabilities of US$9.21b due within 12 months and liabilities of US$11.7b due beyond that. On the other hand, it had cash of US$644.1m and US$1.83b worth of receivables due within a year. So its liabilities total US$18.5b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since General Mills has a huge market capitalization of US$47.6b, so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

General Mills has a net debt to EBITDA of 2.9 suggesting it uses a fair bit of leverage to boost returns. But the high-interest coverage of 8.7 suggests it can easily service that debt. Sadly, General Mills's EBIT actually dropped 4.8% in the last year. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if General Mills can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, General Mills recorded free cash flow worth a fulsome 81% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.”

I’m not a big numbers guy, but in a market that values cash flow and debt structure, it is worrying to see just how debt-heavy GIS is.

Competitors

GIS’ largest competitors include Nestle, Mondelez, Hershey’s, KraftHeinz, and Kellogg’s. It’s not exactly an easy battlefield to conquer. So let’s delve into how these behemoths compare to GIS.

Mondelez

Mondelez isn’t really worried, it has an incredibly solid portfolio of snacks and is even further expanding in comparison to GIS. “Consumer demand for snacks continues to increase, and Mondelez International sees itself as well-positioned to not only meet those needs but increase its market share in the process.”

Nestle

The only issues Nestle is facing are in regards to the health aspects of their products, which GIS is also facing.

“Nestlé says less than half of its mainstream food and drinks are considered ‘health. The annual report of the world’s largest food company showed 54 per cent of its food and beverages by revenue — excluding products such as pet food, baby food, vitamins and specialised medical nutrition — were rated lower than 3.5 under the widely used health star rating (HSR) system. Nestlé claims big win for transparency as it reveals 39% of UK sales are HFSS. Nestlé said it would announce a target to improve its global figures by the end of this year.”

In a fairer world, this would be detrimental to a company, but the reality is this doesn't affect much of anything, with “Nestlé Ranked As Most Valuable Food Brand As Many F&B Brands Grow, Morning Consult, which did its own study on brand popularity, said food and beverage brands snagged 8 of the top 20 slots on its list of fastest-growing brands for 2022, as “low price points appealed to cost-conscious consumers. “In a year of historic inflation, consumers’ tighter wallets impacted purchasing consideration for brands,” Joanna Piacenza, head of industry intelligence at Morning Consult, said.”

Kellogg

Kellogg is GIS’ largest competitor in the brands' fundamental sector- cereal. So looking at how Kellogg performs can give us a very good understanding of how GIS may perform.

“Kellogg's sales and profit beat estimates, to retain plant-based meat business. Americans have so far taken price hikes for snacks and breakfast cereals in stride even as decades-high inflation forces consumers to dial back spending.”

“Kellogg joins other major food and beverage companies, including Oreo maker Mondelez International Inc (MDLZ.O), Coca-Cola Co (KO.N) and Hershey (HSY.N), in using its brand power and distribution scale to pass on price increases to consumers while seeing little pushback in demand.”

KraftHeinz

KraftHeinz is expanding quickly with “Kraft Heinz to use Anheuser-Busch InBev’s B2B e-commerce platform in Latin America Kraft Heinz suggested the move could be the catalyst to help it realise its emerging markets strategy.”

The company also has incredibly high ambitions with the “Kraft Heinz Co. executives see innovation as its chief growth driver in North America and are targeting $2 billion in incremental sales by 2027. To achieve that growth the company will focus on three trends — exploration and authenticity; quick with quality; and holistic wellness.”

Hershey

Hershey has been expanding rapidly, moving from confectionary to savory foods as the next land of conquering. “Hershey purchased Amplify, the parent company of popcorn brand SkinnyPop, for $1.6 billion in 2017, the largest deal in the company’s history. It also acquired Pirate’s Booty cheese puffs a year later, and in 2021 doled out $1.2 billion for fast-growing Dot’s Homestyle Pretzels and its Midwest co-manufacturer Pretzels Inc. The acquisitions have rapidly given Hershey “one of the strongest snacking portfolios” in the salty category, Riggs said, and turned the division into a major revenue generator, contributing about 10% of the company’s more than $10 billion in annual sales. Hershey is aiming to grow its salty snacks division to about 20% of the company’s sales, about $3 billion, within a decade, she said. “It is amazing how quickly we've gone from zero to 10% of sales and getting to the point of scale,” Riggs said. “We really have hit our stride.”

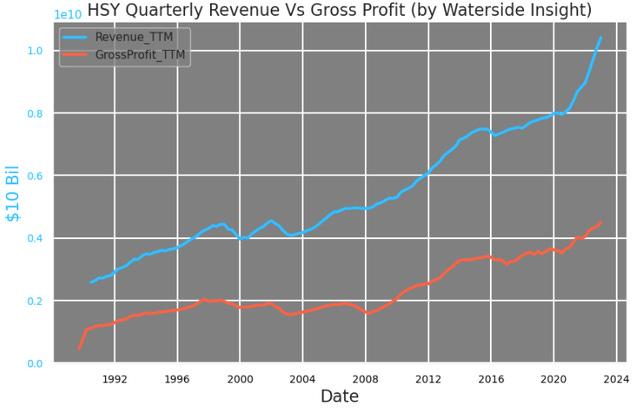

The reality though is that they face the same issues as GIS with the lipstick effect being of large concern for the entire sector. “There is a so-called "lipstick effect" that when facing the stress of economic challenges, consumers would still treat themselves to "affordable luxury" while cutting back on other consumption. Chocolate consumption is part of the affordable luxuries for average consumers. With the looming recession, we want to investigate how resilient the company might be when facing challenges. On top of its long-established brand and reputation, in recent years, Hershey has great balance sheets and cash flow statements to attract investors. Its revenue and gross profit have been at their strongest in its long history.

Looking at this chart with history dated back to 1988, we can see that during the last recession of 2008-2009, the company's revenue almost didn't take many hits, but its gross profit was dented. Could Hershey be recession-resilient this time? To be clear, we are not here to argue against chocolate's incredible power of stress release and delicious taste. The "lipstick effect" generally works for chocolate consumption but is not necessarily enough to help Hershey's bottom line, especially this time. We found the company is facing a similar situation as before '08-'09 with rising costs but less buffer and more elevated stock prices. For one of the largest chocolate producers in North America, Hershey still needs to tighten the belt to brace for some storms ahead. We think the current valuation is too rich, and recommend a sell at this level.”

Investor sentiment

“Long time holder of GIS.. I would like the lower debt to continue and dividend increases to go up after many years of 1 cent increases.. they have done a nice job changing this company in the last 3-5 years and the balance sheet looks better than it has in many years.”

“This is a boring stock.. I have held it a long time..buy it add to it.. when it goes down add as much as you can. I have been pretty happy with GIS over time.. its boring but consistent over 5, 10, 15 and 20 year periods.”

“The pet food acquisition really helped them charge with some growth.”

“These are consumer staples, perhaps it's best to invest in them that way. Don't trade GIS, buy it monthly, have for a great deal of time. My take, these are not trading vehicles. The prices raised on their products might change some customers' purchasing preferences, but will not come down, so, margin increases in the future. Factor in time.”

SWOT analysis:

Strengths:

Resilient to a recession

Mostly long term holders

A diverse profile

Operations in most countries

High return on their stock

Strong customer base

Weaknesses:

Lipstick effect

Debt structure

Competitor strength

Stagnation

Opportunities:

A higher dividend

More share buybacks

Spend more money on advertisement

Produce new flavors of their existing products

Threats:

Recession can cause irreparable damage if the capital structure isnt strong enough

They need to start expanding and innovating if they want to hold their position in a market as competitive as food

Point Game

Estimate:

I’m expecting a 5% change after the report comes out. Over the last couple of quarters, 6% has been the normal change after each report however, I’m expecting a little less change this time due to a decreased trading volume from investors.

Estimate: +5%

Report Time: Thursday before market open

Market Cap: 47,611,065,398

P/E Ratio: 16.86