Marathon Oil

Marathon Oil Long

Overview:

Marathon Oil Corporation is an American company engaged in hydrocarbon exploration incorporated in Ohio and headquartered in the Marathon Oil Tower in Houston, Texas. They began as The Ohio Oil Company in 1887. In 1889, the company was purchased by John D. Rockefeller's Standard Oil. It remained a part of Standard Oil until Standard Oil was broken up in 1911. In 1930, The Ohio Oil Company bought the Oil Company and named it Marathon. It also runs international gas operations focused on Equatorial Guinea. As of December 31, 2022, the company had 972 million barrels of oil, of which 86% was in the United States and 14% was in Equatorial Guinea. The company's reserves consisted of 52% of petroleum, 30% natural gas, and 18% natural gas liquids. In 2020, the company sold 383 thousand barrels of oil per day.

Strategy:

With the foundation of a strong balance sheet and the competitive advantages of their multi-basin portfolio, including the Eagle Ford in Texas, the Bakken in North Dakota, the STACK and SCOOP in Oklahoma, and the Permian in New Mexico, they believe that they have the right portfolio of assets and the right strategy: putting returns first, generating sustainable free cash flow at conservative oil prices and sharing that cash flow with investors.

Understanding the company:

Petroleum is a dark-colored, thick crude oil found deep below the ground in certain areas. The name petroleum means rock oil. It’s called petroleum because it is found under the crust of the earth trapped in rocks. Petroleum is a complex mixture of compounds that is made up of only two elements, carbon and hydrogen.

Formation of petroleum: It is formed by the decomposition of the remains of tiny plants and animals buried under the sea millions of years ago. Their dead bodies sank to the bottom of the sea and were soon covered with mud and sand. Due to high pressure, heat, bacteria, and the absence of air, these dead remains are slowly converted into petroleum. The petroleum formed then gets trapped between two layers of rocks, forming oil deposits.

Extraction of petroleum: It is extracted by drilling holes in the earth’s crust, where the presence of oil has been predicted by special machines. The oil wells are drilled by using drilling rigs. When an oil well is drilled through the rocks, natural gas comes out first with great pressure for a time and the crude petroleum oil comes out by itself due to the gas pressure. After the gas pressure goes away, petroleum is pumped out of the oil well.

Natural gas: It is found deep under the crust of the Earth either alone or along with oil above the petroleum deposit. Some wells produce only natural gas whereas others produce natural gas as well as petroleum oil. It is formed under the earth by the decomposition of the vegetable matter lying underwater. This decomposition is carried out by anaerobic bacteria in the absence of air.

Advantages:

It is a good fuel because it burns easily and produces a lot of heat.

It burns with a smokeless flame and causes no air pollution.

It does not produce any poisonous gases on burning.

It does not leave any residue on burning.

It can be used directly for heating purposes in homes and industry.

It can be supplied to homes and factories through a network of underground pipes and this eliminates the need for additional storage and transport.

Uses:

It is used as domestic fuel and industrial fuel.

It is used as a fuel in thermal power stations.

It is used as a fuel in transport vehicles. It’s a good alternative to petrol and diesel in vehicles because it is a cleaner fuel and does not cause much air pollution.

It’s a source of hydrogen gas needed to manufacture fertilizers. When natural gas is heated strongly, the methane present in it decomposes to form carbon and hydrogen. This hydrogen is then used to manufacture fertilizers.

Customers and partners:

Although Marathon Oil doesn’t make this public, there are strict requirements in order to work with them. Marathon Oil is dedicated to upholding high ethical standards and principles throughout their operations worldwide. In keeping with the Company’s commitment to high ethical standards, it is important that Marathon Oil’s suppliers and other third-party business partners understand and share Marathon Oil’s commitment to ethical business conduct based on their rules.

My thoughts:

This quarter has been going surprisingly well for oil corporations. Even though oil prices are in a decline, most companies are still reporting record revenues, a recent example of them being BP and Shell. I’m expecting a similar report from Marathon. As I have also talked about this in the past, generally speaking, oil companies aren’t affected by inflation due to the product they sell and their customers. At the same time, compared to last year, oil prices have fallen significantly so a higher price isn’t something that would keep customers away. In fact, I believe the fall in oil prices will contribute to their revenue. Last year, when there was a huge spike in oil and gas prices, people’s natural response was to reduce their use. This could range from them turning off their heating system to taking public transport rather than their own vehicle. Fast forward to this quarter, oil and gas prices have hit an all-time low since the invasion of Ukraine.

Many investors see this as a bad thing however, I disagree with them. Even though oil prices have reached a low, they are still around 20% higher than they used to be. I see this as the perfect combination. We have reached a point in the market where customers see this as a good price. A good comparison of this is when a retail store raises the price of something from $100 to $200 and then discounted it back to $120. Psychologically, you would think that you are getting a good deal even though it is still much more than what you used to pay for it without a discount. The same thing is true in the oil industry right now. I believe the reason why these corporations are reporting record profits even though the prices have significantly fallen, is due to high demand matched with a premium price.

Jumping to their natural gas sector, things are also looking bright. This winter was expected to be much colder than the previous ones. One of the main things natural gas is used for is heating. I’m therefore also expecting increased demand from customers. Something else worth noting is that with the start of the new year, there have also been wage increases that in return make heating more affordable and reasonable to use.

I’d also like to talk about the track record Marathon has when it comes to beating the estimates. Ever since 2020, the company has beaten every EPS estimate. This is very important, especially in today’s market. More and more investors are taking out their money from risky stocks and putting them in more consistent ones that they can trust. A very good track record of EPS beats is a good indicator of strong business fundamentals that remain unaffected even during a recession.

Another event that I believe to have had a positive impact on Marathon Oil is the fall of the used car market. Comparing them to last year, some used cars have lost over half of their value as chip shortages are beginning to end and the market is flooded with cars again. This in return has made buying cars much more affordable and most people who were looking to buy a car are jumping at this opportunity. The increased number of cars on the road also means the consumption of more fuel.

One reason that I can think of why I could be wrong is the continued fall of oil prices. Over the last few months, many big companies that have been doing exceptionally well have lost a lot of their value. The reason behind this is due to investors worrying about a recession coming up so they prefer to take their profits instead of risking them. The same could be said about Marathon as oil has already reached its peak price and it’s starting to come down.

Another reason is the winter season being over. As people start to use their heaters less, Marathon’s natural gas sector could also be affected due to decreased demand. This in return would also cause a bad forecast which could have a negative impact on their price.

Going back to their petroleum production, many cars are now beginning to become fully electric. As consumers have also seen the sharp increase in oil pricing, many of them are preferring to buy electric cars instead, especially now that they are much more affordable.

The next worrying reason is that Biden’s administration has been giving a very hard time to oil companies while favoring renewable energy firms. This means that there are much fewer government incentives and support available to them while they also pay a higher tax than they normally should have. This will all cut into their revenue and EPS.

Research:

Considering that most oil companies usually report similar results, it’s worth comparing Marathon oil to its competitors so that we can get a glimpse of what we should be expecting. In the Eagle Ford, some of Marathon Oil’s competitors include BP , Chesapeake, ConocoPhillips, EOG Resources, SilverBow Resources, and Exxon Mobil. In the Williston/Bakken region, Marathon Oil’s competitors include Chord Energy, private Continental Resources, ConocoPhillips, Devon, EOG Resources, Hess, and Exxon Mobil. The company’s largest competitor in Equatorial Guinea is Exxon Mobil.

Exxon Mobil:

Exxon Mobil is a competitor to Marathon Oil in all of the regions where the company has operations in. At first, Exxon appears to be the better stock. It has a current market cap of $446.68 billion. In comparison, Marathon Oil has a market cap of only $17.17 billion right now. So Exxon with its much larger market cap represents an established company that can be viewed as a safer investment in the eyes of investors. However, Marathon Oil hasn’t reached its final price value and there is a big potential for growth in the coming years. Exxon on the other hand doesn’t have much room for growth left and wouldn’t be a good investment, especially during a recession.

ConocoPhillips:

Next, I want to talk about ConocoPhillips. Both Marathon Oil and ConocoPhillips have positives in the form of increasing fuel/oil prices and expanding into the natural gas market and the prospects of more oil well discoveries. The increasing demand for gas and refined products means that again Marathon Oil has that big potential to expand more. Just like with BP and Exxon Mobil, the cost of environmental hazards and declining oil reserves and production are weaknesses in the case of ConocoPhillips. Then there are the government regulations, but ConocoPhillips will be more negatively impacted by pollution guidelines due to a history of pollution accusations.

Chesapeake

Just like Marathon Oil, Chesapeake’s operations are tied to the US and this is a weakness at times. The other big problem with Chesapeake stock is its high debt. For this reason alone, Marathon is a much better stock as it has a strong balance sheet and it’s one of the main things investors look for in an environment like this.

Devon:

Just like in the case of Chesapeake energy, high debt could make Devon Energy a risky investment. Devon Energy had $6.45 billion of debt, in September 2022, which is about the same as the prior year. The cash position is at $1.17 billion, and so its net debt is at $5.29 billion.

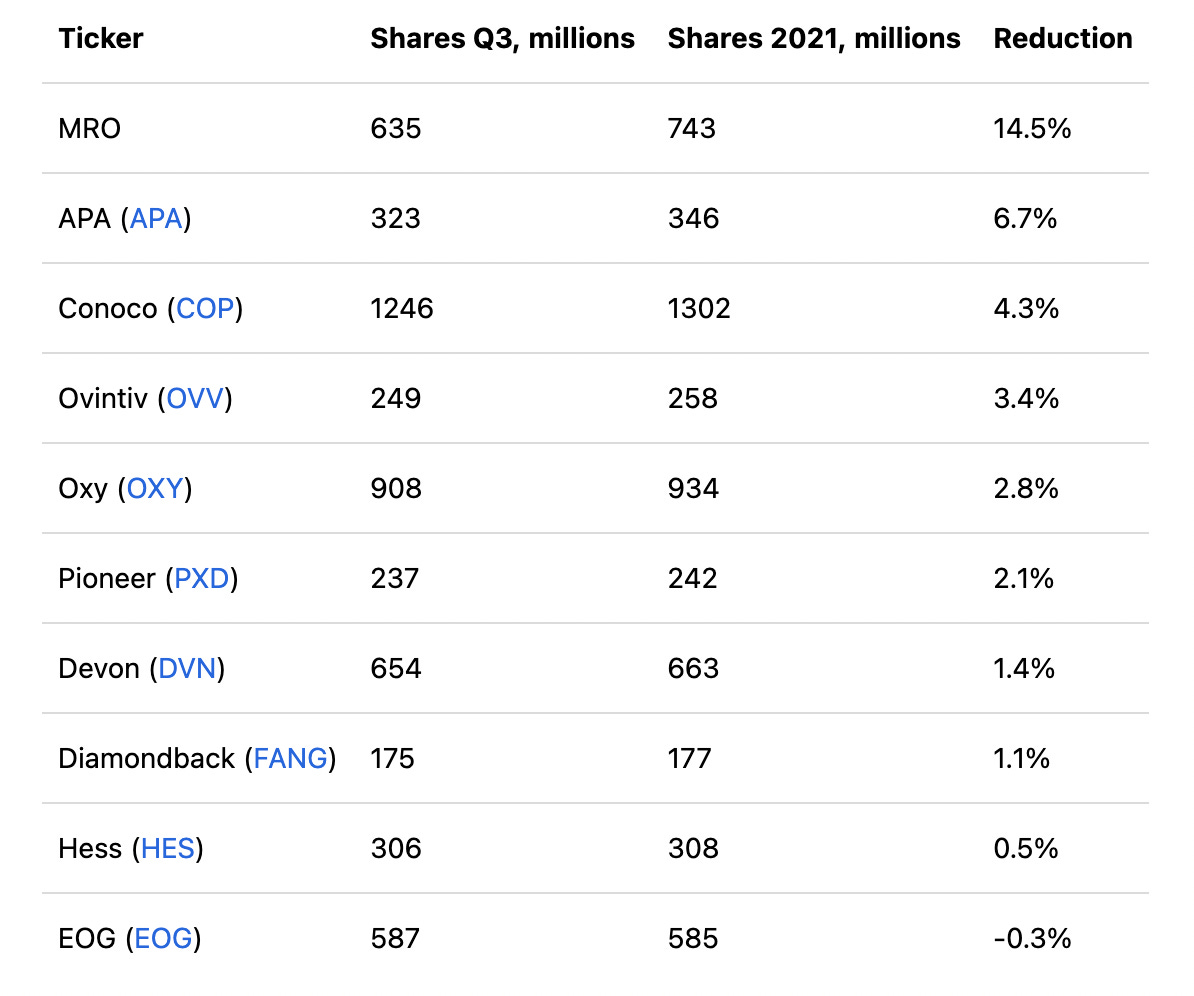

One thing that almost always positively impacts the stock price of a company is buybacks. Marathon is no stranger to this is its share reduction has been over 2x more than their next biggest competitor in buybacks. This combined with their strong balance sheet and low valuation make it a perfect stock to invest in during the recession as it doesn’t have much to lose and is constantly increasing its value.

Their Eagle Ford base is newly acquired. Based on the deal alone, management expects to see a 15% increase in next year's free cash flow, which would result in accelerated share buybacks and an expected increase to $0.10 per share for the quarterly dividend.

MRO received an overall rating of 90, which means that it scores higher than 90% of stocks. Additionally, Marathon Oil Corp scored a 91 in the Energy sector, ranking it higher than 91% of stocks in that sector.

In addition to using excess cash to fund repurchases, Marathon sold its Speedway gas station business in 2021. It received $16.5 billion in cash, which it used to fund $10 billion of repurchases. Meanwhile, Marathon Oil repurchased $3.4 billion of its stock from October 2021 through the end of last year's third quarter. That has decreased its outstanding shares by 20%

I find the share buybacks show their strong business strategies. Most companies try to expand into areas they have no expertise or experience in once they get a big sum of cash. However, Marathon reinvests back in itself and focuses on the one thing they are good at and try to become the best at it.

Shares bought and sold by hedge funds:

What I have also realized is that there have been a large number of shares bought from Marathon over the last quarter by hedge funds. Wellington Management Group LLP grew its stake in Marathon Oil by 1,220.4% and now own 8,754,588 shares worth $219,828,000 after purchasing an additional 8,091,570 shares in the last quarter. Goldman Sachs Group Inc. grew its stake in Marathon Oil by 60.1% and their shares are now worth $194,346,000 after purchasing an additional 2,904,140 shares in the last quarter. Arrowstreet Capital Limited Partnership also raised their number of shares in Marathon Oil by 3,527.3% worth $68,690,000 after acquiring an additional 2,660,158 shares during the last quarter. Encompass Capital Advisors LLC raised its holdings in Marathon Oil by 173.0% in the second quarter and now own 3,794,020 shares of the oil and gas producer's stock worth $85,290,000 after acquiring an additional 2,404,020 shares during the last quarter. Renaissance Technologies LLC raised its holdings in Marathon Oil by 521.5% and now own 2,861,046 shares of the oil and gas producer's stock worth $64,316,000 after acquiring an additional 2,400,700 shares during the last quarter. And finally, BlackRock increased the number of their shares by 3% and now own 9% of the company worth around $700M. 77.30% of the stock is currently owned by institutional investors and hedge funds.

Looking at how big of a position most hedge funds have on this stock, and they own 77% of the shares, I find it to be a very big positive factor. The reason behind this is that these shares are typically bought for the purpose of long-term investments and therefore the chances of a price decrease even after a bad report is minimal. At the same time, every price movement is logical and isn’t based on amateur day traders experimenting. These types of high-value investments also put a big pressure on Marathon as they have no other option but to do exceptionally well, especially looking at how big their competitors are.

Conditions in Equatorial Guinea:

Currently speaking, there is a virus outbreak going on in this country. Equatorial Guinea recently confirmed its first outbreak of the Marburg Virus, a highly infectious and deadly disease similar to Ebola, following the death of at least nine people. Steps to stop this virus from spread followed bu the country quarantining more than 200 people and restricting movement since last week in its Kie-Ntem province. This news is worrisome for investors as if a quarantine is put in place, it will hugely cut into Marathon’s revenue.

I strongly believe that this event won’t have any sort of impact on Marathon’s current price any time soon and is something to be worried about for the future. The reason behind this is that Marathon has its operations going on in Malabo, an island that is completely separated from Equatorial Guinea’s main land and hundreds of kilometers away from Kie-Ntem province. Even if any negative impacts on the stock were caused due to this, it would have been last week when the news broke out and anybody who wanted to sell their shares would have done so by now.

Disadvantages:

Over the last 3 months, EPS estimates have seen 0 upward revisions and 17 downward. Revenue estimates have seen 0 upward revisions and 4 downward.

Devon also came out with their report yesterday. For the first time since 2019, they missed the estimates and delivered very disappointing results due to a decreased demand in oil. This made their stock go down 12%.

With oil prices dropping into a new low and falling below $80 a barrel recently, there is a big risk for Marathon Oil and its investors that the oil and gas exploration company is going to see a continual decline in its free cash flow

Due to rapidly falling petroleum prices in the second half of FY 2022, Marathon Oil’s free cash flow prospects are deteriorating. According to Marathon Oil’s capital plan, the company expects approximately $4.1B in free cash flow this year, of which approximately 25% are reinvested in the business. However, with prices falling below to their lowest in eleven months, Marathon Oil is potentially looking at dramatically lower free cash flow estimate in FY 2023. In the third-quarter, Marathon Oil’s free cash flow already decreased 15% quarter over quarter to $1.13B, suggesting that the firm’s free cash flow and margins have already peaked in Q2 22.

A large part of Marathon Oil’s unexpected free cash flow surge this year has been used to return cash to investors. Since October 2021, Marathon Oil repurchased 20% of its outstanding shares, returning approximately $3.4B in free cash flow to shareholders. A decline in free cash flow, which I continue to expect for FY 2022 due to growing recession risks, may also result in significantly lower capital returns in FY 2023.

Devon Energy said production averaged 636,000 oil-equivalent barrels per day in the fourth quarter. The company’s production was reduced by 2% due to the impact of severe winter weather across its portfolio.

Market sentiment:

“It is undervalued, and has really good growth prospects”

“MRO has during the 12 month period 9/30/21 - 9/30/22 shrunk their FD shares outstanding by 20%. Thus even with flattish production, the lower share count clearly helps EPS growth”

“Production was not sacrificed, its part of the plan. If you ran the #'s my guess MRO would be near the top of the leaderboard for returns”

“ I think that oil prices are headed higher based on the systemic global underinvestment in new oil supply over the past decade combined with the fact that China is now roaring back faster and harder than most people expected. I think that Oil will be close to $100 by mid summer and then stay above $100 for an extended period of time regardless of a potential recession given that almost all of the demand growth is slated to come from developing nations (specifically China, India, & Central America). This is also disregarding the numerous geopolitical risks that could add a negative shock to supply at any given time. There will absolutely be ups and downs along the way, but the reward will be significant for those who buckle up and hold on for the ride. I personally think MRO is set up perfectly to ride the super cycle that we're currently experiencing”

“I think this is a very well managed company and have had a long position since March of 2020. I’m holding”

SWOT Analysis

Strengths:

Low valuation

A high number of cashback compared to their revenue

High dividend pays

Strong balance sheet

Potential for much higher profitability

Weaknesses:

Much bigger competitors

Only operate in a limited number of locations

The price of oil and gas has been on a decline which could affect their stock

Not advertising enough

Opportunities:

Many areas to expand to

Potential to increase the valuation

New countries to build refineries in

Major partnerships with other brands

Threats:

Lower valuations mean not many investors will invest in it

Oil and gas prices are expected to drop which could cause bad forecast

USA wants to increase tax rates on petroleum companies

Many major oil brands that are much bigger and stronger than them

Estimate:

I believe one of the main reasons why my percentage estimate was off on the previous reports was because I was comparing their earnings to past results instead of future results. Thinking about Marathon, while oil prices are expected to go up for the summer, it won’t be by much. Investors are also being extra cautious with their investments. I’m therefore expecting a 5% price movement. Due to most of the shares being owned by hedge funds, a move higher than that is very unlikely. At the same time, the average movement after each report has been around 7% but as people are investing less, it is also natural to have a lower movement. At the same time, it is very typical for Marathon to beat the estimates so there won’t be any surprises to make a big movement.

Estimate: +5%

Time: Wednesday after market close

P/E Ratio: 5.21

Market Cap: 17,202,697,428